MBW Views is a series of exclusive op/eds from eminent music industry people… with something to say. The following comes from Will Page, the author of Pivot, former chief economist of Spotify and PRS for Music, and a fellow of the London School of Economics. Page analyzes the cancellation of 50 (fifty!) music festivals in the UK so far this year, and what it indicates about the live business moving forward.

He says: ‘Recall the adage: Build one too many houses and you collapse the property market? Buckle up, as festivals are now feeling that heat…’

It’s no secret that the Great British summer festivals are finding things tricky this year.

For all the talk of boom-town Swiftonomics at stadiums in Edinburgh, Liverpool and London, for UK festivals it’s carnage with 50 (fifty!) cancellations, and counting.

You’ll find the casualties listed at the foot of this article, but let’s first dissect how we got here.

Around this time last year I offered MBW readers some simple maths for 2022: 2+2=4.

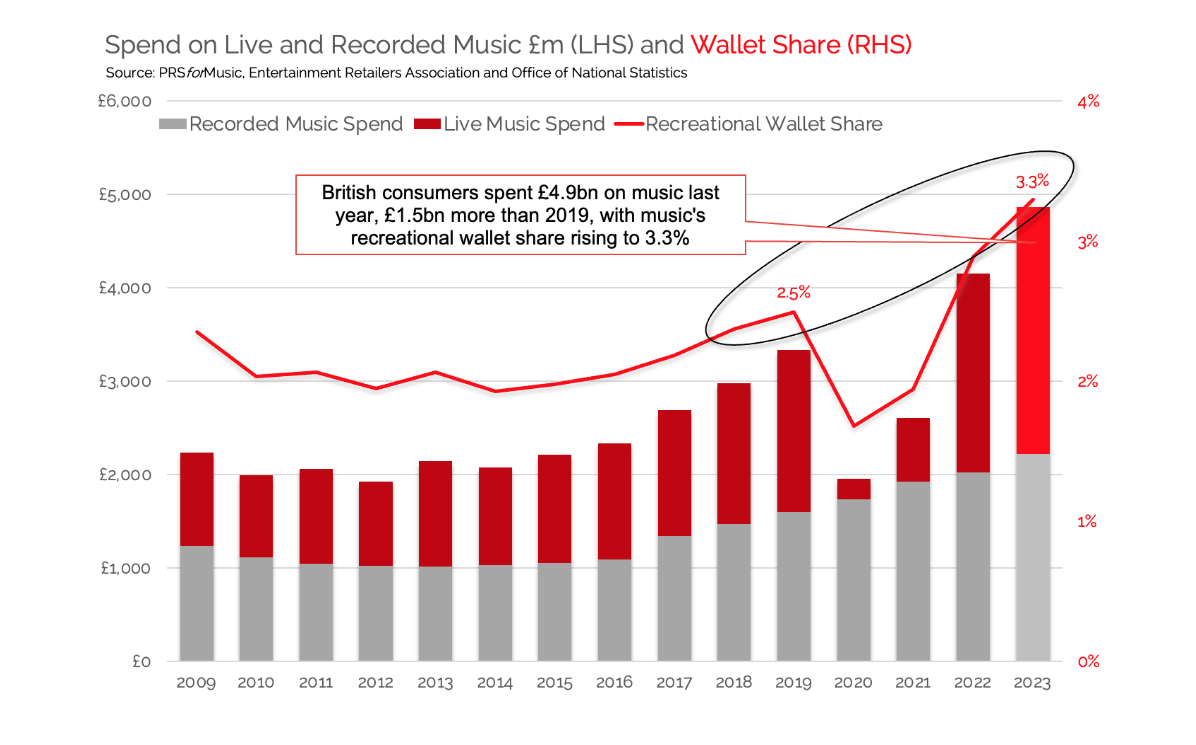

Consumers in the UK spent just over GBP £2bn on live music and £2bn on recorded music, taking the total spend in 2022 to £4.1bn. That was up by almost a billion on pre-lockdown 2019.

Impressed? Now add another £700m in spend across 2023 – 10% growth in recorded and a reported 24% in live – and we’re soaring towards £5bn (£4.9bn, see below).

Not only that, music’s share of consumers’ ‘recreational’ wallet in 2023 rose to 3.3%. In other words, music’s getting a bigger share of a fatter wallet.

And then, the music stopped.

First, there were reports from the US about poor demand for arena tours, where online seating maps reveal to the consumer just how lonely they’ll be inside (#awkward!).

The forces of supply and demand don’t help but there’s a credit crunch hitting festival promoters this year that hurts, regardless of ticket sales.

In many ways, festivals large and small are staring at a triple whammy of Brexit, Covid and now inflation and those costs now forcing upon festival organisers have been simmering for a couple of years and are finally bubbling over.

“The toilet hire for a festival in 2021 was £28,000. Then, for the exact same amount of kit in 2024, we were initially quoted £54,000.”

Millie Devereux, We Are The Fair

We Are The Fair production director Millie Devereux notes: “Budgets have grown exponentially since COVID-19. The toilet hire for a festival in 2021 was £28,000. Then, for the exact same amount of kit in 2024, we were initially quoted £54,000.” Contrast that with the average ticket prices, rising by only 17% from 2019 to present.

Here’s the credit-crunch promoters are currently calculating: you either scale back production, jack up prices or call it quits.

Rostron’s solution is for the UK Government to throw the industry a temporary lifeline and lower VAT from 20% to 5%.

“Lowering VAT can move the needle from loss to profit, as it gives breathing space to their unpredictable and uncontrollable supply chain costs,” he argues. “If they had done this earlier, many of those 50 cancellations would have still gone ahead.”

Issue 2: Supply – an empty field of niches?

One trend is emerging from the cancellation carnage: multi-genre festivals are being hit hard — and if we look at what music consumers are streaming online, the collapse of human editorial, and subsequent rise of the algorithm, may explain why.

Festivals work because we all gather round a main stage late at night and sing the same songs together. If our point of connection isn’t others with pulses (but rather our own unique algorithmic choice) then festivals serve a field of niches that ain’t an easy sell.

“A genre-unfocused festival-poster lineup starts to just look like a playlist that has been made and personalised for somebody else.”

Glenn McDonald

Perhaps we’re not at a point where no single act can sell out a festival. What’s more, lots of different acts confuse the algo-trained consumer. Glenn McDonald, author of the brilliant book You Have not Heard your Favourite Song argues that “a genre-unfocused festival-poster lineup starts to just look like a playlist that has been made and personalised for somebody else”.

Another way to think about this field of niches is to compare a supermarket with a specialist butcher — after all they both sell the same product. Put one K-Pop act on a festival stage and you might sell a bunch of day tickets, book three and you’ve got the biggest K-Pop festival in Britain.

If we are staring at a field of niches, it would stand to reason that artists and festivals with a clear USP will weather the storm. Take the soul-and-jazz focussed Love Supreme Festival who do just that — where demand held up nicely this year.

Issue 3: Demand – go really big or stay home

Richard Kramer (co-presenter of the Bubble Trouble podcast) reminds us how bubbles get into trouble when we “get over our skis”. Stadiums and Festivals have exploded in volume and value, capturing half of UK box office in 2022 (up from a fifth ten years prior), which might explain why their skis hit the skids.

Why? Gig goers had money back then, they’ve less now and with inflation rooted into the ticket and all that surrounds it, they’re spending less of it. What’s more, much of it will be spent on Taylor Swift.

It’s not a race to the bottom, it’s a race to the top – people draw up priorities for their spend (e.g. holiday, city break, dining out, favourite act and festival) and when they rationalise, the most expensive wins. This applies to festivals and restaurants alike

This taps into a headline from last year, ‘go big or stay home’; consumers are willing to spend hundreds on stadium shows, but not spare change on grass roots. One reason why can be found hidden in my book Pivot — and, for this, we need to think retail.

Chris Gardener, of commercial realty giant CBRE, argues that nobody goes into shops anymore and asks: ‘Have you got … ?’

If there’s a perceived risk it might not be in stock, they default to Amazon. Perhaps a stadium de-risks the experience too?

Issue 4: Culture – Socials don’t socialise in fields

An increasingly common response from those who went to festivals in the past but chose not to this year is that ‘they didn’t think they had friends to go with’. Ouch! I’m not equipped to unpack this one but I’ll try to help you do so by pointing out two things.

First, social media may result in what Amazon’s Katie Vitolins referred to as a ‘claustrophobia of abundance’. They may have hundreds (or thousands) of friends online, but that doesn’t translate into human interaction in festival fields.

Second, remember the target market for many of this year’s festivals – school leavers (18-19 years) and graduates (21-23 years) — these age buckets were caught in the awful cross-fire of the 2020 pandemic. Healing that wound may still be a work in progress.

“Fans with tattoos of their favourite band or those able to recite lyrics word-for-word… has way more meaning than any data dashboard.”

Putting angst about future generations aside, another consideration is that the internet, which I’ve long argued can scale just about anything other than intimacy. Promoters must have a wry smile when labels debate the definition of ‘superfan’.

Looking for superfan signals in a pro rata pool of streaming data is meaningless.

Marty Diamond, a legendary booking agent, once told me that the only data point he trusts is comments-per-views ratio. Lots of views with no comments translates to a lot of ‘meh,’ but lesser views accompanied by a higher ratio means a lot of engaged fans.

For promoters, not only do they have the issues of price and scarcity to juggle, but they can also visibly count those fans with tattoos of their favourite band or those able to recite lyrics word-for-word. That has way more meaning than any data dashboard.

Issue 5: Just blame the weather

Lastly (as we in the UK know too well) It’s pissed down for the first half of 2024. Or to put a more factual spin on it, we had a top 20% wettest March, the sixth wettest April of the last 189 years and well-above average rainfall in June. That’s got to affect the choices being made by the consumer.

“WizzAir will get you [from the UK] to Lisbon for £29.99.”

Elena Joseph

“Less money, more choice,” remarked social commentator Elena Joseph. “Reading is asking for a three-figure number that begins with a three (£325 a ticket), whereas WizzAir will get you to Lisbon for a two-figure number that begins with a two (£29.99)”.

She concludes “Younger generations who are tired of British weather may bide their time and then opt to save-and-go-south where the sun will definitely be shining this summer”.

So, now what?

The commercial real estate world coined the expression ‘earn back the commute” — you can’t just expect workers to come back to the office, you need to earn their respect by offering more convenience and amenities.

So how do festivals “earn back” the concert-goer?

It ain’t going to be easy. I can quickly cough up a list of alarming headwinds: disposable income is tightening while inflation is reeling (and pushing more of us into higher tax bands) and the expiry of favourable mortgage rates looms like a ticking time bomb.

But festivals are countering this with tailwinds of their own, like investing in supermarkets on site with cheap(er) beer for those who want to party, whilst also switching focus to offering yoga. pilates and wellness centres for those that don’t.

If offices can do it, so too can festivals. The time for a rethink begins now.

Keep It Real Folk Festival. Festival cancelled. Reason unknown, appears to be a licensing rejection.

The Summer Solstice Festival. Licence refused in days prior to event after residents hearing

Geronimo Festival. Cancelled with two months to go. “The event has become an unsustainable financial risk.”

ZenFest. Cancelled for 2024. No suggestions it will return.

Starry Village. Cancelled one month prior to the festival. “Rising inflation has led to production costs drastically spiralling – and the cost of living crisis has had a impact on ticket sales, as folks struggle to make ends meet. Unfortunately, this has led to the very difficult and sad decision that it is just not viable for Starry Village to continue.”

Underneath The Stars. Announced festival will be the last, for now. “This decision, though difficult, feels right as we embrace these new chapters in our lives.”

Another World Music Festival. Postponed until 2025 due to low ticket sales and licensing issues.

Beacon Festival. “The Beacon team have had to make a tough decision in light of skyrocketing festival expenses : Beacon Festival 2024 will be the last.”

Askern Music Festival. Postponed until 2025 after 2024 event is refused licence due to safety concerns.

51st State Festival. Postponed until 2025. “Due to the cost of living crisis, a significant increase in operational costs and operational issues, as an independent festival it is not economically feasible for us to proceed in 2024”.

Towersey Festival. Announces this year’s edition, its 60th, will be its last. “Like many other independent and grassroots festivals we have faced too many forces outside of our control which have made it increasingly difficult to operate and survive”.

Twisted Festival. Postponed after losing their site, and unable to secure new site in time. Intend to return in 2025.

Bingley Challenge Festival. Cancelled three days prior to event “they said “safety concerns”, including fencing off a woodland area in case of fire, had prompted the event’s cancellation.

El Dorado. Cancelled for 2024. “Over the past year we, like many others, have battled with a dramatic rise in operational costs for running a show like El Dorado, compounded by the impact of the increased cost of living on the festival industry and our community. Despite our best efforts we are faced with the potential for catastrophic losses.”

Welliestock. “I have tried for months to reduce the cost of the event but sadly, with everything being far more expensive than 2018 I have not been able to find a way which would have seen tickets having to double in price, something which we always aimed at avoiding as we always want it to be an affordable family event.”

Visions Festival. “Taking a much-needed break for 2024”.

Riverside Festival. “Lower-than-expected sales and increased infrastructure, staff, transport and artist costs”.

We Are Fstvl. Festival cancelled over safety concerns.

Heartwood Festival. “Festivals have lifecycles that rely on the humans that facilitate them, and whilst we’re only in our 4th year our circumstances and aspirations for the future personally, professionally and geographically, won’t allow us to pour the love into Heartwood that it requires”.

ND Festival. “Due to investment and sponsorship changes the festival is no longer viable”.

Meadowfest. Couldn’t reach agreement with landowner. “Never say never but it would be difficult to bring the event back once it has been pulled like this.”

Penn Fest. Cancelled due to trading conditions and increased costs. May return in 2025.

Illusive Festival. Have announced their 2024 edition will be the last.

Clun Green Man. Cancelled due to weather. Will return in 2025.

Askambury Festival. “It’s time we took a break”.

Shindig. Have announced this year’s event will be its last. Cite venue changes and challenges of running an independent festival.

Tunes On The Bay Festival . Has been postponed until 2025.

Lowedefest. Bought to an end after 13 years.

Neighbourhood Weekender. No event planned for 2024. Said they will return in 2025.

Camp Quirky. Taking a fallow year. Cite challenges of running an independent festival.

Doonhame. Rising costs force cancellation of festival.

Splendour. No event in 2024 due to tender and procurement issues. Festival hopes to return in 2025.

Love Fit. Festival cancelled and company goes into liquidation.

Hayloft Live. Cancelled due “to unforseen circumstances”.

Ampthill. Festival cancelled unable to cover costs. company goes into administration.

Connect. Festival will not go ahead this year. No reason given. Suggests it may return in 2025.

110 Above. Rising costs mean no festival in 2024 and no plans for a future edition.

Standon Calling. Festival postpones until 2025.

Spring Classic. Festival cancelled due to costs.

Smoked and Uncut. Festival cancelled. No reason given.

Takedown Festival. Postponed until 2025. Building works and trading conditions given as reason for postponement.

Detonate Festival. Cancelled for 2024 due to costs.

Togfest. No plans for festival to return. Loss of core team and some venue issues given as reason.

Nibley. Announced 2024 will be their last festival. Cite increasing costs against a backdrop of cost of living crisis.

Bingley Festival. No plans for festival to return. “Production costs have gone through the roof”.

Escape Into The Park. Festival will not take place due to “increase in supplier and artist costs”.

NASS Festival. After its 2023 edition it announced it will not return.

Field Maneuvers. Has announced its 2024 edition will be its last in its current form.

Nozstock: The Hidden Valley. Has announced 2024 – its 26 edition – will be the last event, citing rise in supply chain costs as its reason for reluctant closure.

Bluedot Festival. Has said itʼs taking a ‘fallow yearʼ for 2024.

Leopallooza. Made its 2023 edition its final event.

Barn On The Farm. Has announced it will be trying to return in 2025.